{kind=link}

The Association of Healthcare Providers (India) has advised its member hospitals in north India to stop settling claims made by Bajaj Allianz General Insurance in the cashless mode from 1 September. If implemented, Bajaj Allianz policyholders would have to pay at the hospital and later file a reimbursement claim with the insurer, the payment for which typically takes up to a month.

AHPI, in its order earlier this month, said it was considering similar action against Care Healthcare. The standoff underscores the persistent tension among the three key stakeholders in this space—hospitals, insurers and policyholders.

The immediate tussle here is between hospitals and insurers providing health insurance. AHPI members want Bajaj Allianz to increase reimbursement rates for health procedures. They want Bajaj Allianz to pay the amounts they quote and not undercut them while settling claims. Bajaj Allianz, in its statement, fired from the shoulders of policyholders, battling for their right to receive quality healthcare at fair rates. Meanwhile, policyholders are caught between higher premiums from insurers and rising healthcare costs in hospitals.

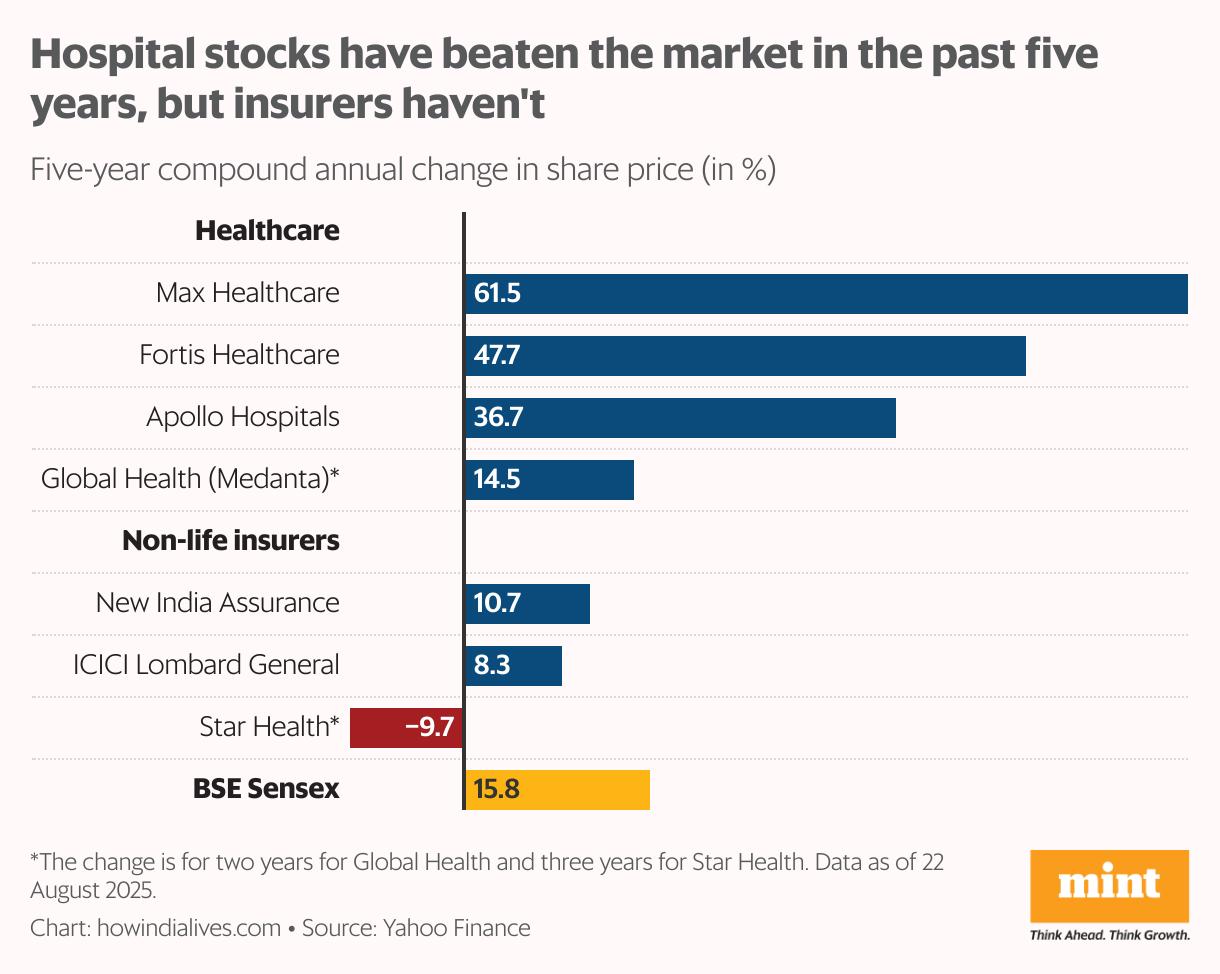

In the last five years, leading listed hospital chains have posted good revenue and profit growth, and higher margins. The covid pandemic marked the start of this period, and provided a business boost to both private hospitals and health insurance. In general, hospitals have grown faster than a small set of listed non-life insurers.

This is also reflected in stock prices. In the past five years, healthcare stocks have beaten the market handsomely, even as non-life insurers have struggled to do so.

Rising claims

The health insurance space is presently serviced by 26 non-life insurers (for whom health is one of the many segments) and seven standalone health insurers (health being their sole segment). In 2024-25, health was a ₹1.18 trillion segment by gross premiums, accounting for 39% of all non-life business, as per the General Insurance Council. In the last five years, it has been the fastest-growing non-life segment, recording a compound annual rate of 18%.

But insurers are facing cost challenges in their health portfolio. The key metric here is net incurred claims ratio—for every ₹100 an insurer receives as premium, how much it pays out as claims. A figure less than 100 is essentially profit for the insurer. Public sector insurers were always in the red. But private insurers, as a set, have gone from 80-84 in pre-covid times to 87-89 even after covid. And standalone health insurers from 58-63 to 62-65.

Premium inflation

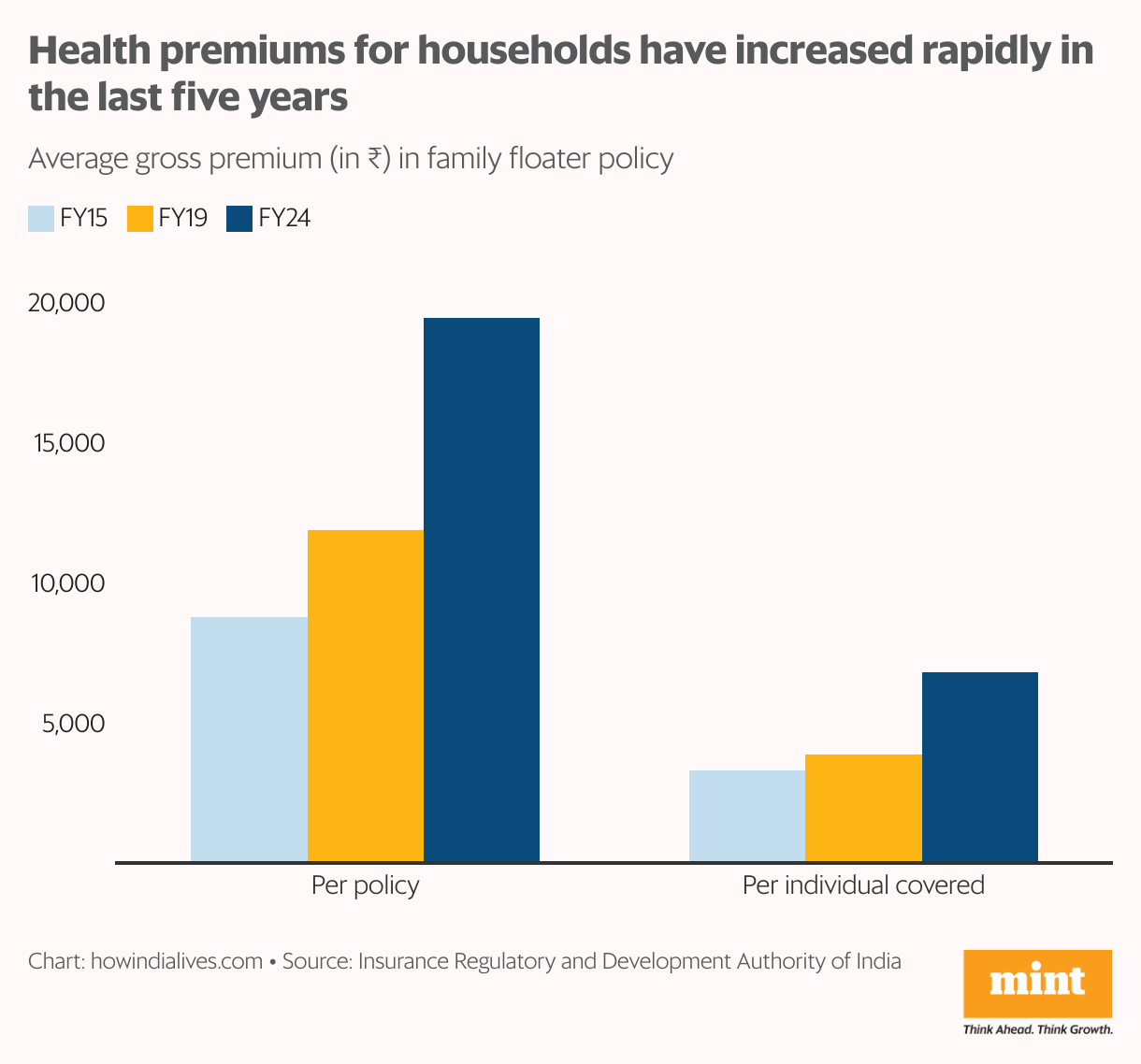

To stay profitable, they have been hiking premiums for policyholders, while trying to strike better deals on procedure costs with hospitals. The biggest segment for them is group insurance (51.7% of gross health premiums in 2023-24). Margins are thin here, but this is bulk business, and so insurers covet it. A further 38.5% comes from households, via two kinds of plans: family floater (28.6%) and individual (9.9%). This is where individuals feel the inflationary brunt.

In 2023-24, the family floater plan—where an individual buys a policy, but it also covers members of their family—covered about 45 million people, against 10.5 million covered by individual policies. Between 2014-15 and 2018-19, the average gross premium per family floater policy increased by 8% annually. Between 2018-19 and 2023-24, this increased 10.3%. At an individual level, the increase in 2018-19 and 2023-24 has been 11.9%.

Cash woes

This increase in premiums is at a portfolio level and doesn’t factor in age. In general, health premiums increase with age. Between 2018-19 and 2023-24, amid the impact of covid, the number of family floater plans increased from 8.7 million to 15.8 million, at a compound annual growth rate of 12.7%. There is likely to be a skew from the younger population in this incremental addition. In other words, the increase in premiums for older age groups is much higher, which is also borne out anecdotally.

Besides rising premiums, if AHPI goes ahead with its directive, Bajaj Allianz policyholders will now have to face process pains and cash flow issues in settlement. Over the years, cashless claims have become the norm, accounting for about 58% of claims and 66% of the claim amount in 2023-24. Even if the insurer and hospitals reach a settlement, as they are likely to, the tension between these three stakeholders will stay.

www.howindialives.com is a database and search engine for public data

Health Insurance India,Hospital Insurance Conflict,Cashless Claims Issue,Healthcare Costs India,Health Policy India,Insurance Premiums,Hospital Reimbursement Rates,hospitals vs insurance companies in India,why hospitals are stopping cashless facility,health insurance claim settlement issues

#trilemma #Indias #health #policy